WELCOME TO COVENANT WEALTH STRATEGIES

Let us help you on your Financial Journey...with our exclusive 8 step "Meaningful Transformation" S.Y.S.T.E.M.

... just know we are not "winging-it" like so many others out there today,

(unfortunately 95% of all policies written are incorrectly, either through ignorance or greed)

Neither are EXCUSABLE !!!

Take our 10 question / 100 Point Financial Quiz to see where you are "at"

....Only by knowing where you're "at" will you know how to get to where you're going!

Life Insurance Has Changed!

Financial Success in a S.Y.S.T.E.M.

Trusted Business Planning Since 2008

Commitment to Your Financial Well-Being

State & Federal Retirement Specialist

Retirement Planning / Estate Planning / Wealth Transfer / Business Exit Strategies

A Team of Experts at Your Service

Pension Maximization

Educators & 403(b) answers

Annuities & Max-Funded IUL

How LIVING BENEFITS Work!

SERVICES

We Provide Growth Consultant Services

We offer specialized retirement strategies, including:

>> Retirement income analysis strategies

>> Personal Tax optimization strategies

>> Business Tax optimization strategies

>> Business Exit Strategies

What is an ANNUITY?

PRO-ACTIVE PLANNING

Our comprehensive financial planning services, offered at no additional cost, empower clients to assess their current financial situation, set clear goals, and develop a detailed plan to achieve them. We specialize in retirement planning, investment strategies, budgeting, and debt management, ensuring a holistic approach to your financial well-being.

We help prepare clients for a financially secure retirement without compromising their lifestyle goals.

What are the PROs / CONs of a 401k?

If you have a match from your employer for a 401k it is a great investment. The potential downsides are:

- Limited Investment Choices: Investment options are limited to what the plan provider offers, which may not always include the best-performing funds.

- Fees: Some plans have high administrative and management fees, which can eat into investment returns over time.

- Withdrawal Restrictions: (Before age 59 1/2) are subject to a 10% penalty and income taxes, with a few exceptions (e.g., Financial Harship, Certain medical expenses, 72T distributions)

- Required Minimum Distributions (RMDs): Participants must start taking distributions at age 73, which can affect tax planning and retirement income.

- Contribution Limits: Although high, contribution limits may still be insufficient for those needing to catch up on savings or aiming for a very high retirement goal.

- Market Risk: Investments are subject to market fluctuations, which can result in losses, especially during economic downturns.

Does an IUL "Implode"?

If a policy is NOT structured and funded properly, it will eventually FAIL. Unfortunately, 95% of all policies are written incorrectly, often due to ignorance or greed, neither are EXCUSABLE!

Does a 401(k) "Implode"?

A 401(k) itself doesn't "implode," but mismanagement or market conditions can lead to significant losses or reduced growth. Key risks include: taken from the 2009 October 19, Time Magazine

- Investment Risk: Poor investment choices or market downturns can lead to significant losses.

- Insufficient Contributions: Not contributing enough, or starting too late, can result in inadequate savings for retirement.

- High Fees: Excessive fees can erode the growth of your investments over time.

Do I have access to my money in an IUL?

Yes, If the IUL is structured PROPERLY then you can have instant access to your money.

Is an IUL FLEXIBLE?

Yes, you can over-fund (up to Govn't regulations) during the "feast" years... and just pay the minimum policy premiums during the "lean" years... AND you can "catch up" the premiums from the years that you didn't pay....

14 questions to Ask your Agent

1.What is TEFRA, DEFRA & TAMRA, and how do they impact my policy?

A: (Your IUL specialist should be able to answer this off-the-cuff. If they say “Let me check on that”—they’re not likely prepared to help structure your policy correctly. Make sure to crosscheck their response with information in Section I, Chapter 7)

2. Explain to me Internal Revenue Code, Sections 72(e), 7702, and 101(a). And what changes to Section 7702 went into effect in January of 2021?

A: (Again, your financial professional should be able to easily explain this to you. If not, beware)

3. What’s a Guideline Single Premium?

A: (This is the total amount you will put into fully fund, or self-insure, your policy)

4. What factors will the insurance company consider when gauging the size of my policy, besides the Guideline Single Premium?

A: (This includes your age, gender, and health status)

5. What size policy would someone have (on average) who is a non-smoking sixty-year-old with a GSP of $500,000?

A: (It’s approximately a $930,000 to $1,050,000 death benefit)

6. What are the rules for perfecting a modified endowment contract?

A: (60 Days after the next policy anniversary date of the policy) Section I, Chapter 7 Creating a MEC

7. How can an insurance company earning 4% to 5% on their General Account Portfolio afford to credit a policy 5% to 10%?

A: (By linking to an index where the insurance company buys upside options with the interest on your principal—but your principal is preserved)

8. How can policyholders experience 1% to 2% higher pay-outs than the average index that they are linked to?

A: (By using Alternate Loans where the interest charged might be 4% to 5% and the cash value is being credited a higher rate, such as 7%)

9. Who runs your policy illustrations?

A: (Ideally, your financial professional, familiar with your individual circumstances and objectives, should design your illustrations, not a third-party insurance company)

10. If I maximum fund an IUL LASER Fund, over the life of the policy, what is the expected net internal rate of return likely to be - compared to the gross crediting rate - if the historical average were 7.5%?

A: (Usually around 1% different—which would be 6.5%. See Section I, Chapter 9, Figure 9.2)

11. How long have you been structuring these types of policies? Do you have access to several different types of IUL policies, and how many have you put in place?

A: (Hopefully they’re not brand new to the strategies)

12. Do you specialize in maximum-funded Indexed Universal Life policies, or do you handle other types of insurance, as well?

A: (Let’s hope this is an experienced answer, or at least your financial professional is with an experienced firm who can support him/her in partnering with you)

13. How many insurance companies do you represent? Do you work for only one company or are you an independent producer representing multiple companies?

A: (Remember, while not imperative, independent producers can have an advantage in ensuring you get the optimal policy for your situation, as well as upgrades down the road)

14. Is insurance your sole profession, or is it a part-time endeavor?

A: (Ideally you want someone who is dedicated to this full-time, not juggling it with other types of work)

What is Pension Maximization

Pension maximization means making smart financial decisions to grow and manage your retirement savings effectively. It includes choosing the right investments, minimizing taxes, and planning withdrawals wisely. This ensures you have enough money to live comfortably when you retire and stop working. It's like optimizing a long-term savings plan.

What Does LASER Fund Stand For?

Liquid Assets Safely Earning Return

What is F.I.R.E.?

Financial Independence Retire Early

What is ARBITRAGE?

(earning a spread on the money you borrow)

(borrowing at one rate and earning at a higher rate)

example: Borrowing at 5% and still earning 7.5% on the accumulation value.

These are critical benefits that can empower you to move forward toward your financial and retirement goals.

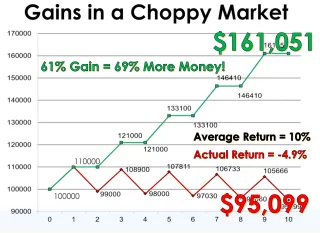

If the Market drops 50% then gains 50%.....

This is the MYTH of Wallstreet!

In order to Break-Even:

a 25% Loss has to be followed by a 33% Gain

a 33% Loss has to be followed by a 50% Gain

a 50% Loss has to be followed by a 100% Gain

What are the Advantages of an IUL over a ROTH

A ROTH HAS 2 ADVANTAGES:

-ACCUMULATE tax-free

-WITHDRAW your money income tax-free

A LASER FUND HAS AN ADDITIONAL 4 ADVANTAGES

-LARGER contribution

-LIQUID (no penalties)

-SAFTEY from market loss

-BLOSSOMS income tax free

How does Indexing Work?

With STOCK OPTIONS... if the Market goes UP you gain...

if the Market goes DOWN the options expire and you don't loose a penny of principle

Pursuit of Excellence Promise

A professional strives for more than competence. The professional has discovered that he or she will accept nothing less than excellence in the work they do for their clients. Because they accept nothing less than excellence, they will actively work to learn what they did wrong if they fall short of excellence.